Banking and Debt Cycles

The modern banking system can trace its origins to the early days of the Renaissance, in Northern Italy. There, in affluent trading cities such as Florence, Venice, and Genoa, traders dealing solely in finance would set up a bench (called banca in Italian- where the modern word bank comes from) financing voyages, engaging in arbitrage, and funding ship-building for merchants. Banks of that period dealt almost exclusively in gold and silver coins, and traded these coins freely for foreign coins stamped by a different King. They quickly realized that dealing in physical coins was costly, burdensome, and dangerous, as thieves would often rob money-laden wagons between towns.

So, they came up with an innovative solution. Instead of handing over coins to their customers, they would ask that the customer place their gold or silver in the bank’s vault, which already stored the bank’s own money, and in return the bank would hand them a banknote, or a physical receipt of ownership of the gold. The customer could then take this note and pay for real goods or services someplace else instead of carrying the coins.

The banks quickly saw a loophole– no one was auditing their vaults, and comparing how much gold was there versus how many notes the bank had issued. The financiers immediately began to issue more notes than gold in the vault. This system would work fine as long as every customer had confidence in their banknote and believed that the gold backing their coins was actually there. But, once the bank started facing financial troubles, and customers showed up to redeem their notes for gold, a bank run would immediately begin- with many clients ending up with worthless pieces of paper after the vaults were emptied. Authorities created extreme punishments for bankers caught issuing more notes than gold in the vault – in some places in Medieval Italy, death penalties were enforced for bankers caught issuing too many notes- in others, life in prison was the punishment.

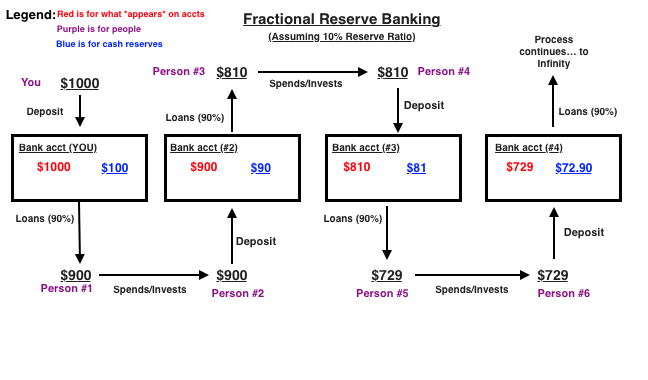

Our modern financial system is based on the early Italian antecedents. Most people believe that when you deposit funds into the bank, the money stays in your account. In reality, the funds you invest are immediately lent out, re-deposited, and lent out again. This is called Fractional Reserve Banking. Thus, the “money” you see in your bank account is a lie. It isn’t really there. Let’s break down how this works. Say you earn $1000 from a recent paycheck. You go to your bank and deposit these funds. The next day, the bank takes $900 (90%) of the cash you deposited and loans it out, keeping 10% in reserve in case you come to withdraw some of it. This money is given to Person #1, who takes this loan and buys some paint for his house. The vendor who sold him the paint then takes the $900 received and deposits it in the bank. The bank then repeats the process, loaning out 90% of the money, or $810 to Person #3, who spends/invests it with Person #4, who deposits it again, and the process repeats. Here it is visualized:

All along the way, the bank is able to take the same dollar bills and re-loan it out through multiple transactions (a la rehypothecation), and charge interest on the loans it creates. This is essentially a near- infinite money glitch in the system, and allows banks to make exorbitant profits, like JP Morgan making over $12B in Q4 2020 alone. However, this process also serves to GREATLY increase systemic risk- in the example above, one single $1000 transaction is turned into what APPEARS as $3,439 in bank accounts, but is actually just credit, re-deposited and re-borrowed over and over again.

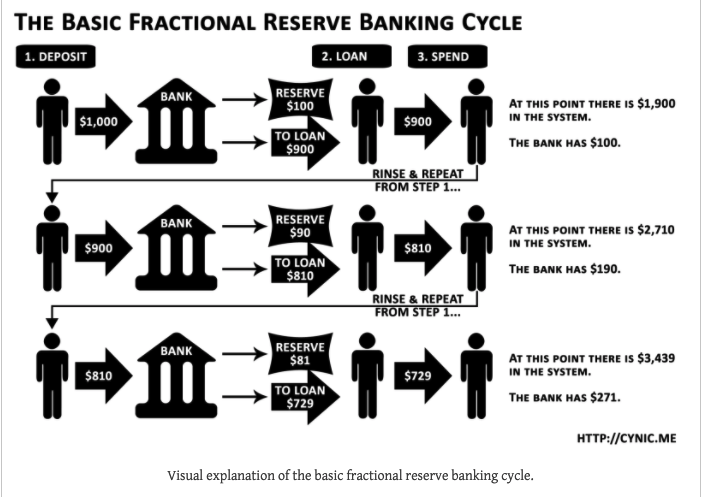

Here’s another way to visualize it:

Typically, the majority of a banks’ capital provided to businesses will be business loans, lines of credit, or venture financing. These business loans will be put to work to expand factories, build new products, hire workers, or create intellectual property- generally things that expand economic growth.

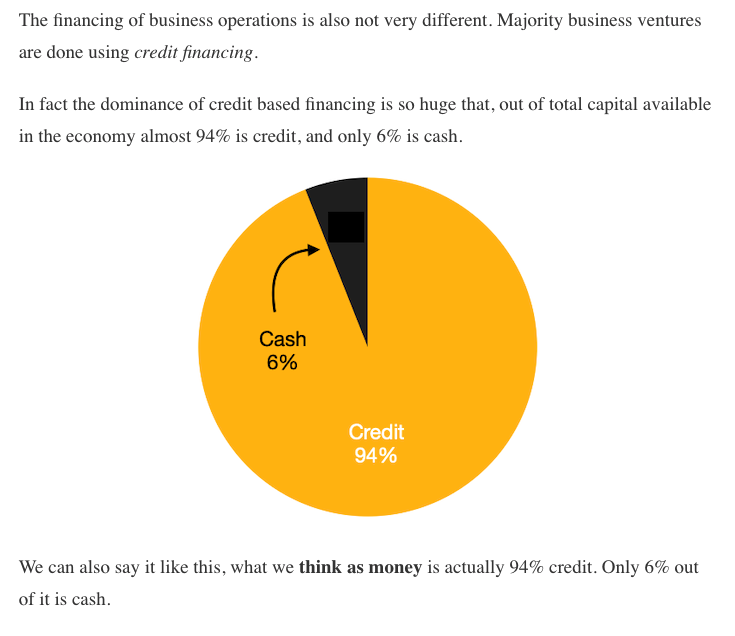

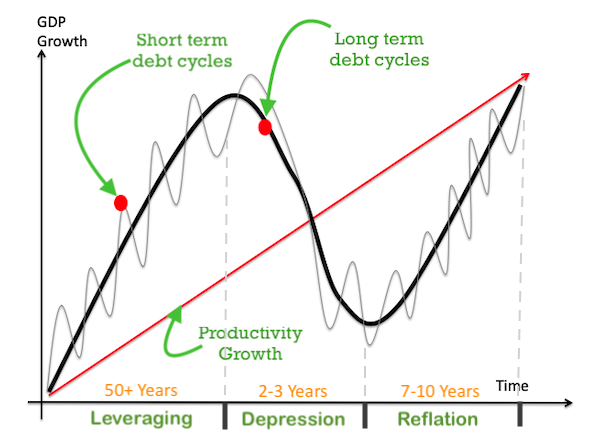

This effectively means that the vast majority of what we “think” of as money, is not cash, but credit. Most funds in the system, thus, exist in the form of debt. Another effect of Fractional Reserve banking is a supercharging of the debt cycle. Because banks are allowed to loan and re-loan cash that is deposited, banks are able to create massive amounts of credit, helping to boost economic growth in the boom stage, and worsen economic decline in a bust. The Debt Cycle is a economic phenomenon that has been observed for centuries- in ancient Israel, for example, the state enforced a debt “jubilee” every fifty years (a long human lifespan) to dissolve all debts, release people from bondage, and restore ancestral lands to the descendants. There are two main cycles- the long term “super” cycle, which lasts between 50-80 years (longer in countries with higher life expectancy, so most developed countries this is 80 years) and the short term “normal” cycle, which occurs every 8-10 years or so.

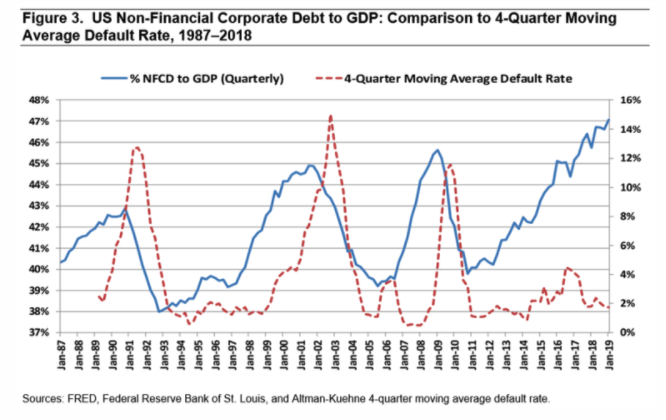

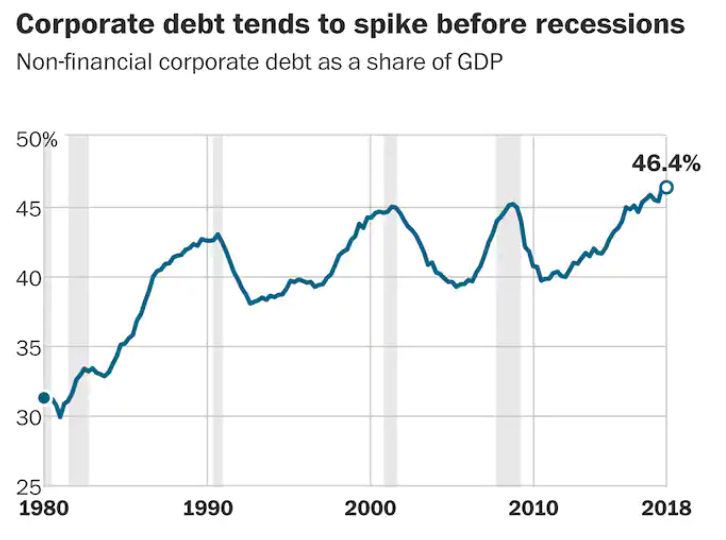

Look at the US as an example. As you can see below, when we continue through the expansion phase of the credit cycle, companies borrow more debt to invest in new products or services. Once a recession hits, many of these businesses are forced to de-lever (pay back debts) and those which aren’t able to de-lever, go into bankruptcy. (notice we are LONG overdue for a recession and bankruptcy spike)

The Great Depression

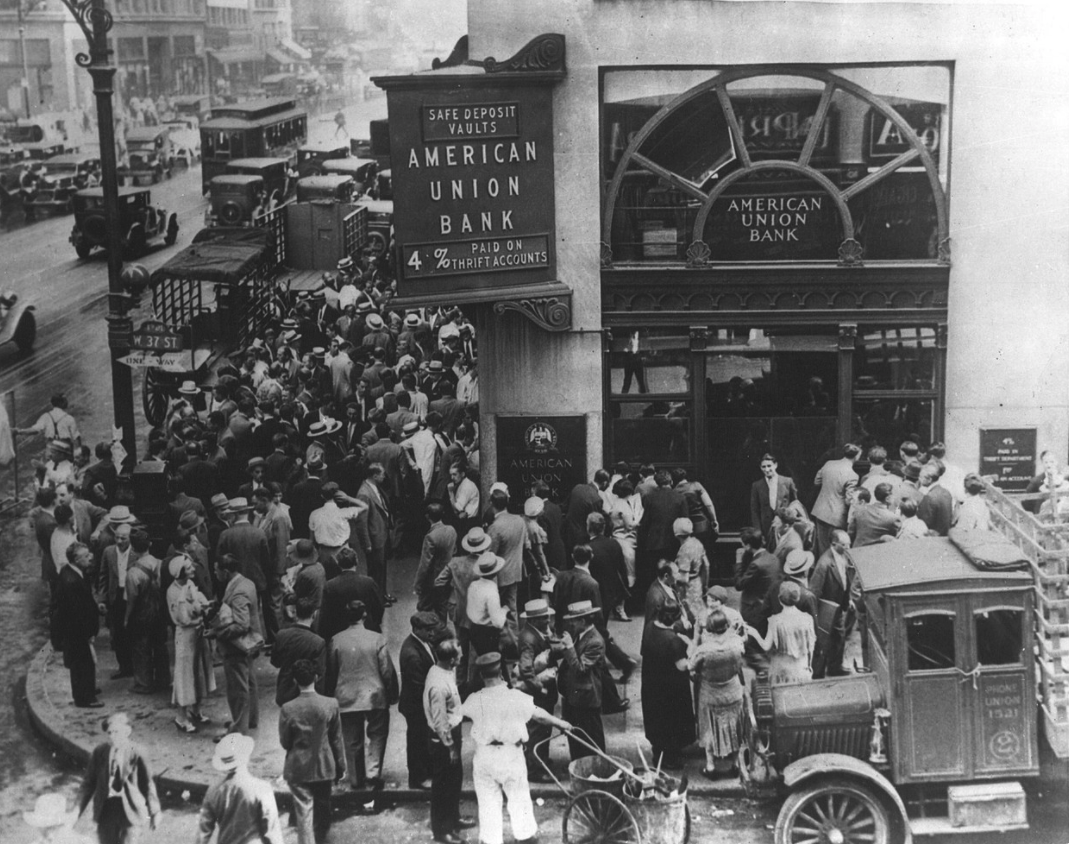

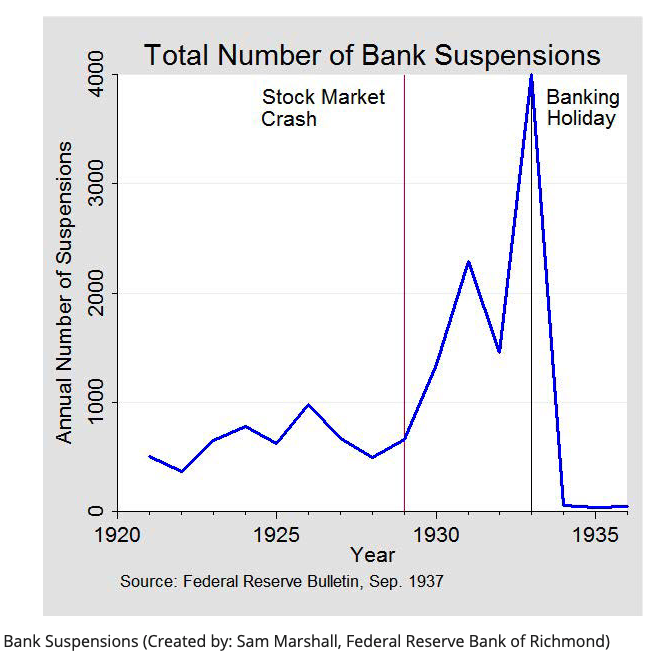

The last debt supercycle began cresting in the 1930s. The US appeared to be poised for economic recovery following the stock market crash of 1929, until a series of bank panics in the fall of 1930 turned the recovery into the beginning of the Great Depression.

When the crisis began, over 8,000 commercial banks belonged to the Federal Reserve System, but nearly 16,000 did not. Those nonmember banks operated in an environment similar to that which existed before the Federal Reserve was established in 1914. That environment harbored the causes of banking crises. One cause was the practice of counting checks in the process of collection as part of banks’ cash reserves. These ‘floating’ checks were counted in the reserves of two banks, the one in which the check was deposited and the one on which the check was drawn. In reality, however, the cash resided in only one bank. Bankers at the time referred to the reserves composed of float as fictitious reserves (again, rehypothecation anyone?). The quantity of fictitious reserves rose throughout the 1920s and peaked just before the financial crisis in 1930. This meant that the banking system as a whole had fewer cash (or real) reserves available in emergencies.

Another issue was the inability to mobilize bank reserves in times of crisis. Nonmember banks kept a portion of their reserves as cash in their vaults and the bulk of their reserves as deposits in “correspondent banks” in designated cities. Many, but not all, of the ultimate correspondents belonged to the Federal Reserve System. This reserve pyramid limited country banks’ access to reserves during times of crisis. When a bank needed cash, because its customers were panicking and withdrawing funds en masse, the bank had to turn to its correspondent, which might be faced with requests from many banks simultaneously or might be beset by depositor runs itself.

On November 7, 1930, one of Caldwell’s (a large financial conglomerate that lost millions in stock market speculation) principal subsidiaries, the Bank of Tennessee closed its doors. On November 12 and 17, Caldwell affiliates in Knoxville, Tennessee, and Louisville, Kentucky, also failed. The failures of these institutions triggered a correspondent bank cascade that forced scores of commercial banks to suspend operations. In communities where these banks closed, depositors panicked and withdrew funds en masse from other banks. Panic spread from town to town. Within a few weeks, hundreds of banks suspended operations. About one-third of these organizations reopened within a few months, but the majority were liquidated (Source). Businesses that relied on loan financing started to collapse, and unemployment started to climb.

What followed was a protracted period of bank runs and panics lasting for years. Contrary to common belief, not all bank runs happened at the same time- some banks experienced one or two runs- others more than that. The Great Depression was a series of panics, rather, that culminated in a near-complete collapse of the banking system and a ban on gold as legal tender by FDR in Executive Order 6102. In the wake of the crisis, several key financial reforms were made. Among them were the creation of FDIC (Federal Deposit Insurance Corporation) which was created in 1933 to “insure” bank deposits with government funds. This, it was hypothesized, would stop bank runs and restore confidence in the system. Another reform was the creation of the Glass- Steagall Act, a key legal provision that forced commercial and investment banks to remain separate entities.

However, both of these in time would serve to further increase risk, not reduce it. The FDIC, for example, insured $100k (later updated to $250K during 2008) of bank deposits. This was supposedly done for the benefit of the client, but many overlook that it also greatly benefited the bank. When you deposit cash into a bank, it is an asset to you- but to the bank, this is a liability- it represents a cash amount that they will have to pay out to you upon your request. By insuring the deposit, the bank gets essentially free insurance on their liabilities, which allows them to justify taking more leverage. Glass- Steagall’s separation of banks was an amazing step at reforming the system- sadly, it was repealed in 1999 by Bill Clinton under the Gramm–Leach–Bliley Act (GLBA). Commercial banks are where you deposit funds, get mortgages, small business loans, and personal lines of credit- Investment banks are firms that underwrite financial transactions, create derivatives, and speculate in the market.

By combining the two, banks are essentially allowed to bet with depositors’ money- and if they fail, they can rightly justify to regulators that their collapse would end in financial calamity for millions of working-class depositors who would lose everything since their accounts would be suspended. Thus, they become “Too Big to Fail” and receive Federal Govt bailouts, no matter how reckless they have been.

The Money Illusion

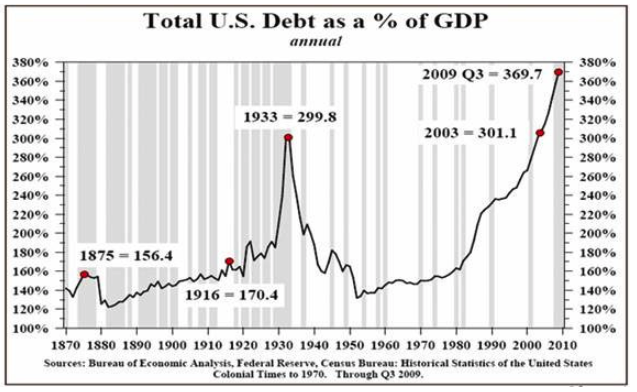

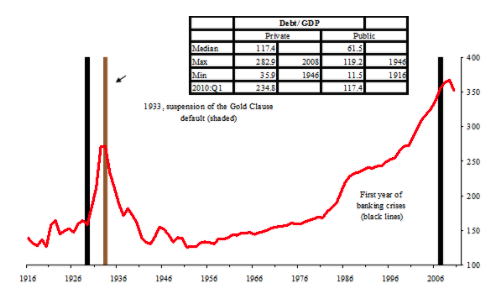

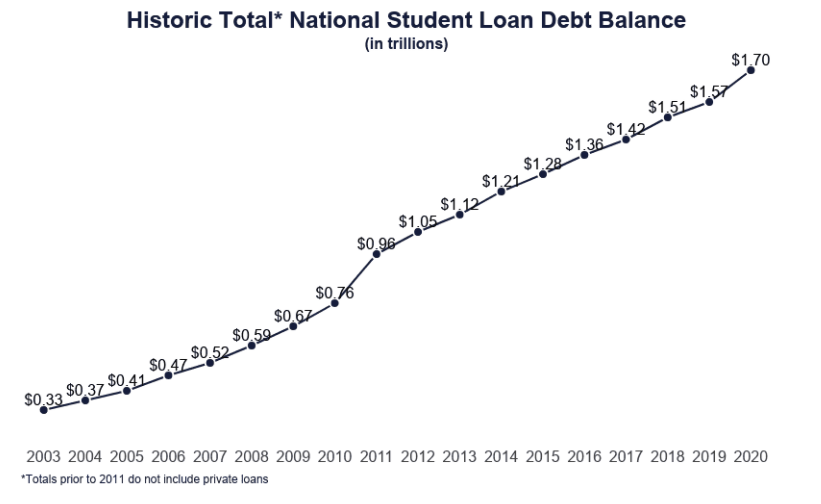

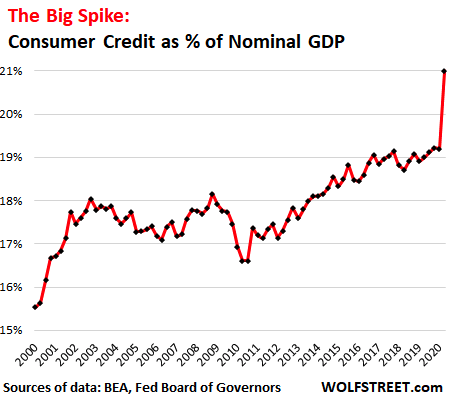

In 2008, we were at the end of a major debt supercycle. The frenzied mortgage lending and securitization in the financial sector, along with massive consumer credit borrowing, had set the U.S. up for a major crisis. In relative terms, we were at a 27% HIGHER total debt to GDP ratio than the Great Depression.

These massive debt loads were coming home to roost, manifesting first as a crisis in subprime but then quickly moving to prime mortgages, corporate debt markets, money markets, and even the consumer credit markets.

But, this didn’t happen. Ben Bernanke, the Chairman of the Federal Reserve, was a self avowed student of the Great Depression- and was determined not to let it happen again. He, along with Treasury Secretary Hank Paulson (Former CEO of Goldman Sachs) and Tim Geitner, created new lending facilities and MBS purchase programs in order to swallow the massive amounts of toxic assets the system had created.

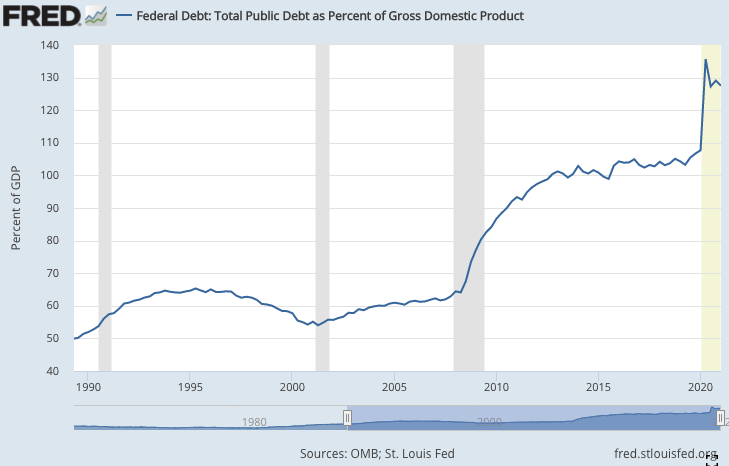

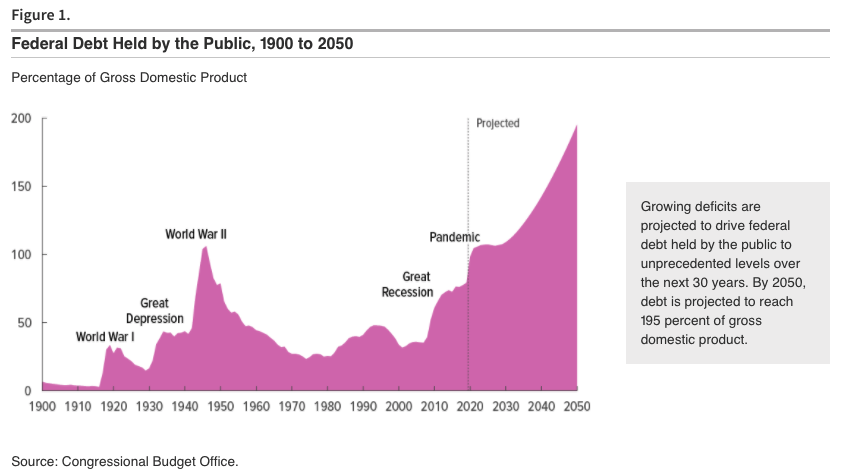

Paulson and Bernanke technically had no legal authority to create these programs, but in a crisis, all caution goes out the window. TARP and other programs authorized by the Treasury bought billions of dollars of MBS, funded by T-bond issuances. This chart shows US Govt Debt as a % of GDP through today: (notice the spike in debt during and after 2008)

The US borrowed heavily- TARP alone was authorized for $700 billion. The Treasury did not have the funds to support this so it issued billions of dollars of T-Bonds. Banks, hedge funds, other governments, and the Fed all bought these bonds en masse.

Remember, only the Treasury has the ability to SPEND, and only the Fed has the ability to LEND/PRINT. The Fed was created as a private institution to “protect” the government from reckless money-printing. The Primary Dealers (banks approved to trade directly with the Treasury) buy government bonds from the US Treasury, and turn around and sell these bonds to the Fed or other third parties. If you’re confused about how the system works, I recommend watching this video on how the financial system functions.

In the equity markets, as we started bottoming in the first quarter of 2009, hedge funds, banks, and family offices began loading up on margin debt again. This renewed confidence in the banking system and overall lending capacity began pushing equity markets back up.

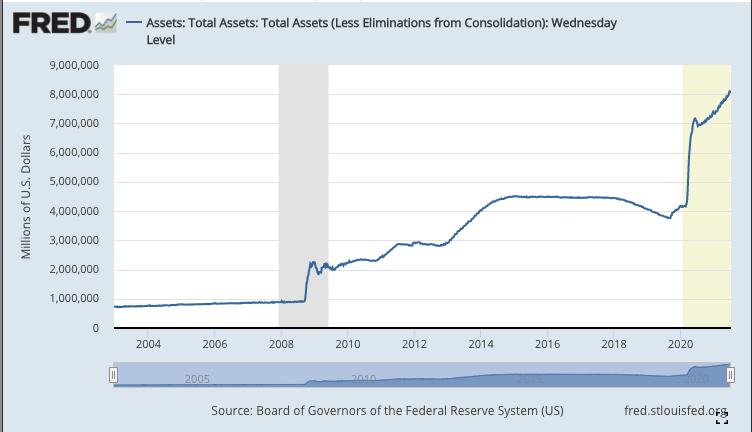

Further stabilizing the markets was the Federal Reserve with their massive Quantitative Easing program. In 2008, the Federal Reserve’s Balance Sheet ballooned– assets grew from $880 Billion pre-crisis, to $2 Trillion immediately after, and eventually over $4T by 2014. Many economists, particularly those with a libertarian bent, such as Peter Schiff, immediately decried this reckless behavior and predicted hyper-inflation as early as 2011.

When the Fed buys assets, it is completely different from any other institution buying. Pension plans or mutual funds use the savings of the investors of the fund. Because that money came either from working, or from other investments, it represents NO net increase in money supply. The money they received HAD to come from someone else, for a good/product/service/asset they created or provided. However, the Fed has no taxing authority, no savings, no funds to speak of at all- EVERYTHING the Fed buys it purchases through money it PRINTS. Thus, Fed Balance Sheet expansion=money printing. The Fed printed $2T in the two years following 2008.

This rampant money printing rightly worried experts and pundits in the media- but the inflation they feared never came. They were flat out WRONG. Why? Most of the new money that was printed went directly into the banking system. Lyn Alden describes it brilliantly-

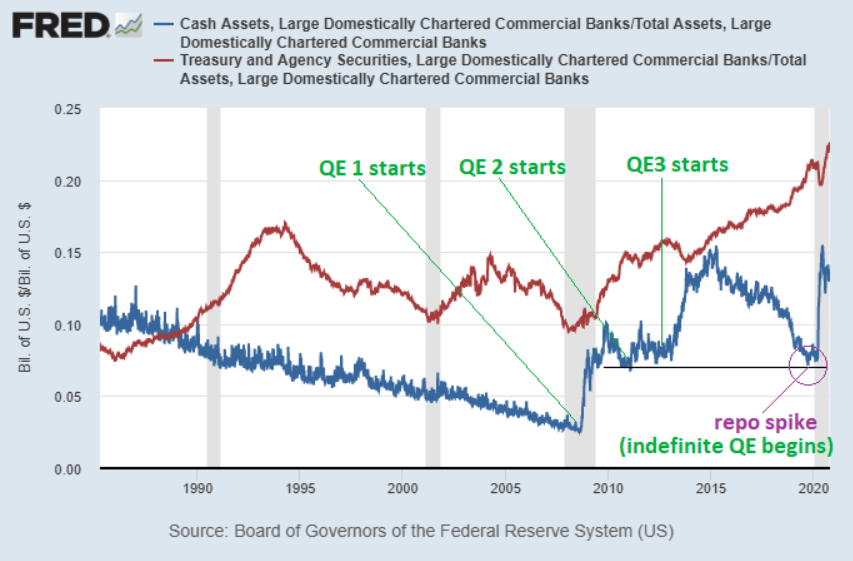

“Leading into the financial crisis, only about 13% of bank reserve assets consisted of cash (3%) and Treasury securities (10%). The rest of their assets were invested in loans and riskier securities. This was also at a time when household debt to GDP reached a record high, as consumers were caught up in the housing bubble.

That over-leveraged bank situation hit a climax into the 2008/2009 crisis, coinciding with record high debt-to-GDP among households, and was the apex of the long-term private (non-federal) debt cycle. When banks are that leveraged with very little cash reserves, even a 3% loss in assets results in insolvency. And that’s what happened; the banking system as a whole hit a peak total loan charge-off rate of over 3%, and it resulted in a widespread banking crisis” (Source).

Thus, the new money went to recapitalize banks and shore up their balance sheets to defend them from bankruptcy- it stayed in untouchable bank reserves, and never entered circulation. The money that didn’t go to repair bank balance sheets flowed directly into the markets.

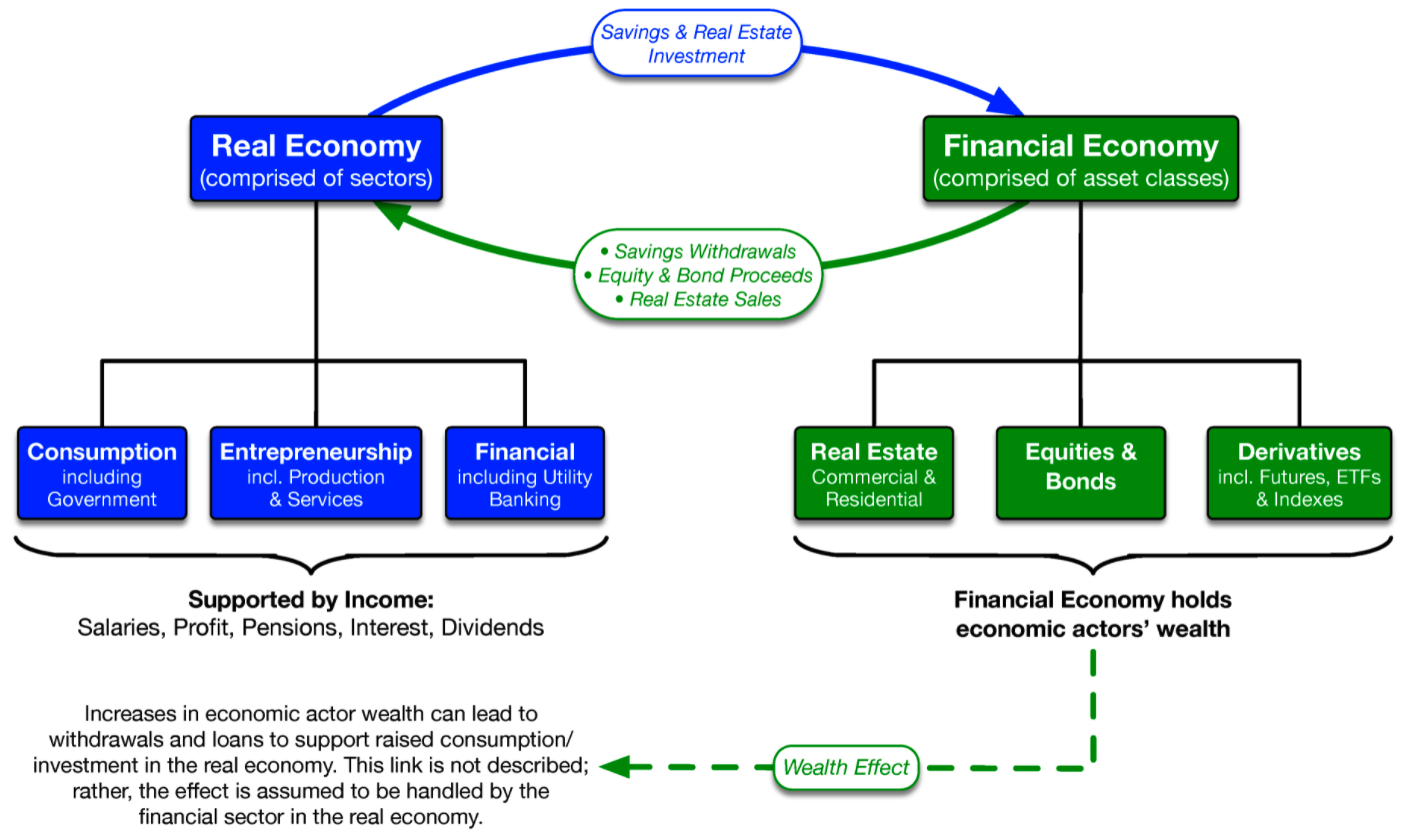

There are two different economies- the real economy, and the financial economy. The tidal wave of new money the Fed was creating did not cause inflation (in the traditional sense), because the money did not flow into the real economy- the goods, products and services that everyone consumes on a daily basis. The money instead flowed into the Financial economy- bond markets, stock markets, private equity funds, commodities, Forex markets, etc. (if you’re still confused, please read this article)

When you give a bank $100M, it doesn’t go out and buy $100M worth of Big Macs and Kleenex- the bank puts these funds into investments, generally either in the form of loans or in the form of equities or equity derivatives. Thus, the funds that flowed into the banks are stored up almost exclusively in the financial system, or get pushed into loans to consumers.

“Wait a second!”- you say. “The Fed printed money to buy T-Bonds- The Treasury usually spends funds that go into the real economy– so THAT should have caused inflation, right?”

Yes, this is typically what happens. But, during and after the 2008 financial crisis the majority of new Treasury expenditures went to programs that were stabilizing the financial system (TARP+ TAF+ TLGP+ Others). So, the money that would have been spent by govt agencies in the real economy instead just flowed back to banks and financial institutions.

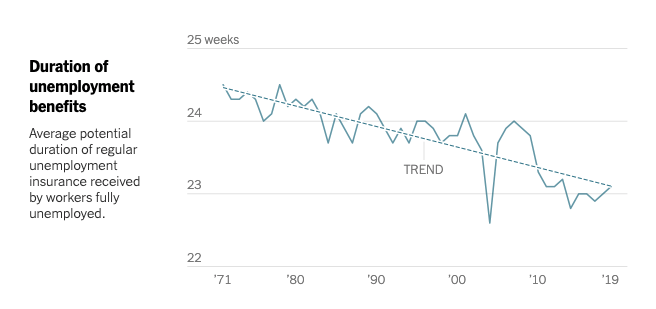

Typically in a recession the Treasury will increase spending to cushion the blow to workers- and in 2009 they did extend a few unemployment benefits. But, by and large, Congress authorized few benefit programs for workers, and the average time on the benefit decreased after a slight bump in 2009.

Thus, the amount of freshly-printed money that reached the real economy was minimal, and whatever money did reach it largely acted to counteract deflationary forces- it wasn’t enough to actually induce inflation. The government did little to stop foreclosures, or provide aid to small businesses. Unemployment spiked, and due to the Phillips Curve Principle (covered in Pt 1), this put a dampening effect on inflation.

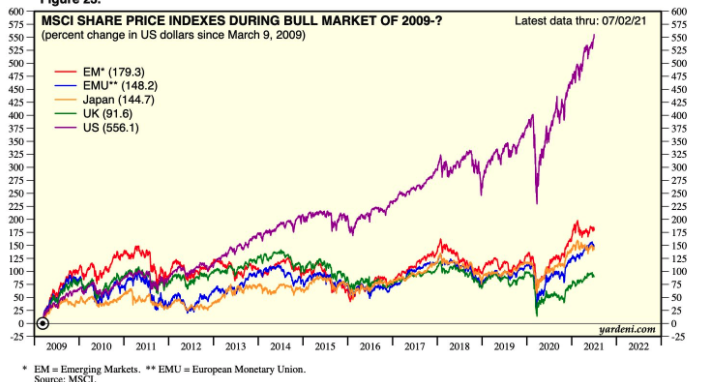

The funds the Federal Reserve had created, therefore, created no inflation in the real economy- instead they flowed to the financial economy and inflated financial assets. This started off the largest and longest bull market run in U.S. Stock market history– easily beating emerging and other developed countries’ equity markets.

Keynesian economists lauded this as an accomplishment- they believed they were creating what is called a “Wealth Effect” – a theory that stated that as people’s financial wealth increased, they would be induced to do more spending and investment- thus, by propping up the stock market, they would stimulate the real economy. This is awfully convenient for the rich- the top 10% own 85% of the equity markets, and thus have seen their wealth balloon by over 186% while growth for everyone else stagnated.

Ironically this theory has it exactly backwards- real economic growth should drive the stock market, not the other way around. But, convinced of their theories, economic policymakers continued to pump ever increasing sums into the financial system.

When you divide stock market performance by the Fed’s Balance sheet, you see that there has been basically NO real growth since 2008.

The entire “rally” we have experienced for the past 12 years has been nothing but an illusion- it is simply the result of vast money inflows into the financial system. Banks and financial institutions will do everything they can to convince you that the high stock market valuations are justified by fundamental growth.

This is wrong- these valuations are NOT justified. Insane levels of money printing and debt leverage have created extremely dislocated equity markets. For example, Square (SQ) has a forward PE ratio of 499.87- it currently doesn’t pay a dividend, but let’s assume it paid a 3% dividend payout ratio (which is rare for tech stocks) – if that were the case, it would take 14,996 YEARS for the dividends to pay pack the price of ONE SHARE. (449.87/0.03).

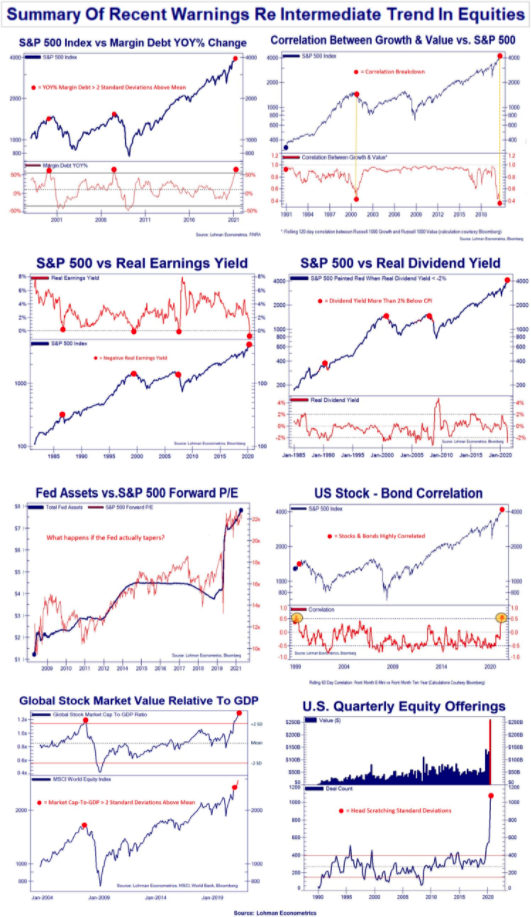

To summarize, see this image from a post I made a month back- all the warning lights are blinking red. The markets are at the extreme end of the range by almost every valuation metric- and no one seems to care.

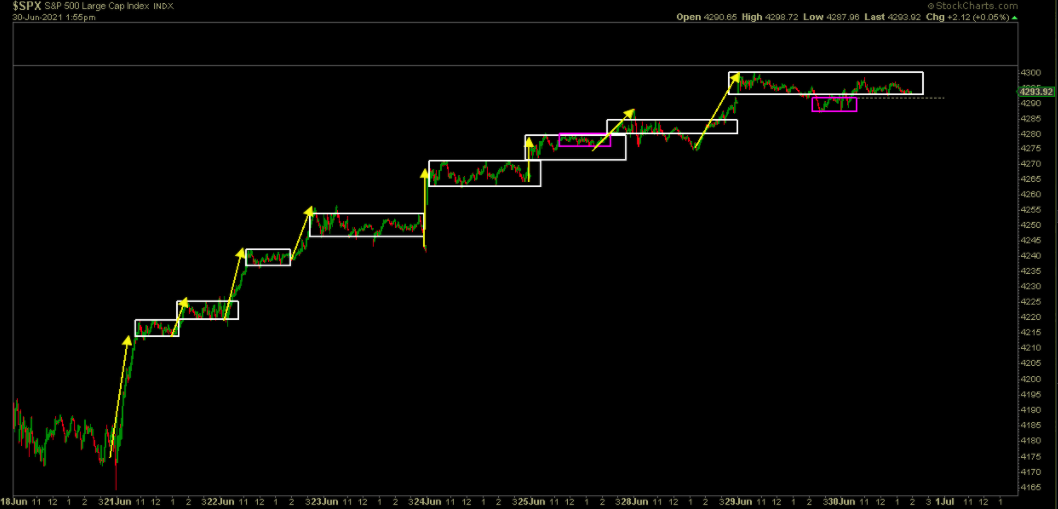

The markets are slowly being “walked up” every day. Today, the ultimate price insensitive buyer (the Fed) is now plowing $120B a month into Treasuries and MBS, and the Primary Dealers now have to turn around and put their money somewhere. The bond market is already a trap with 2% yields, and 5% inflation. There’s no more profit potential there, so these institutions are forced to buy equities if they want any returns. The Fed is killing whatever is left of price discovery.

Four billion dollars or so a day is being pumped into the system- and going straight to the stock markets.

Further, to stimulate growth in the real economy, policymakers dropped interest rates to near 0% in late 2008 to induce bank lending to get consumers to borrow and spend again. (70% of our economy is consumption due to the factors discussed in Part 1).

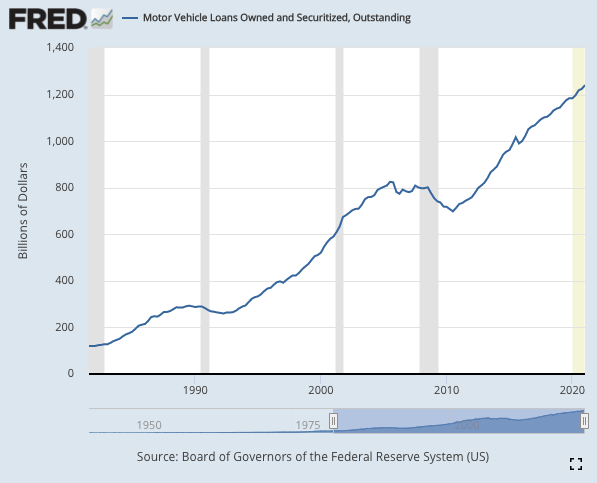

This did create massive loan demand- basically every sector of the US economy began borrowing en masse. The Fed was able to “reflate” the bubble and allow the economy to survive on debt financing to “re-invigorate the economy”. Fast-forward to today, and a decade of pinning rates to the zero-bound has us breaking records in terms of debt loads:

I could go on and on, but you get the point. Now, the entire system is overleveraged- the cancer has spread, and it has infected virtually every single sector of the economy.

People keep saying that we “kicked the can” of 2008 down the road. This is WRONG. We kicked the can UP THE STAIRS- meaning, we not only delayed the problem, but made sure it would get WORSE, since we borrowed MORE to paper over the old debts and worthless securities the system had created.

A fascinating aspect of our recent financial history is that the bailouts are exponentially growing– this is due to the simple fact that the entity giving the bailout has to have a balance sheet multiples larger than the firm receiving the bailout, and government guarantees of banks induce reckless speculation. For example, to bailout a bank with $10B in mark-to-market losses, you need a bank with a $20 or $30B capital surplus, to absorb the loss and keep the depositors and creditors satisfied that the bank giving the bailout won’t go under.

In 1998, a hedge fund called LTCM was near collapse- it had leveraged itself over 25-1, using complex algorithms made by Nobel Prize winning economists to predict bond prices. They had made massive derivative bets buying Russian bonds (among other things) – and when the Russian government defaulted in August 1998, their positions began to unravel. The massive debt and derivative exposure they had created was threatening to pull several large banks down with it. The Fed stepped in during September to organize a $3.5 Billion bailout, funded by 12 large banks. According to James Rickards, General Counsel of the LTCM Bailout- the US equity and bond markets were “close to being completely shut down” during the worst of that crisis. (start at 16:30)

In 2008, the entire US financial system was nearing collapse and desperately needed a bailout. A massive bank run had begun. Congress stepped up and provided- in the end spending over $498 Billion of taxpayer funds. However, the Fed also provided a bailout (though QE), eventually buying over $1.7 Trillion of MBS.

Since the Great Financial Crisis, the banking system debt crisis has now become a government debt crisis, and indeed an economic debt crisis- and this debt has spread worldwide. Equity and bond markets have continued to march up, despite fundamentals. This new financial paradigm was rightly termed “The Everything Bubble”

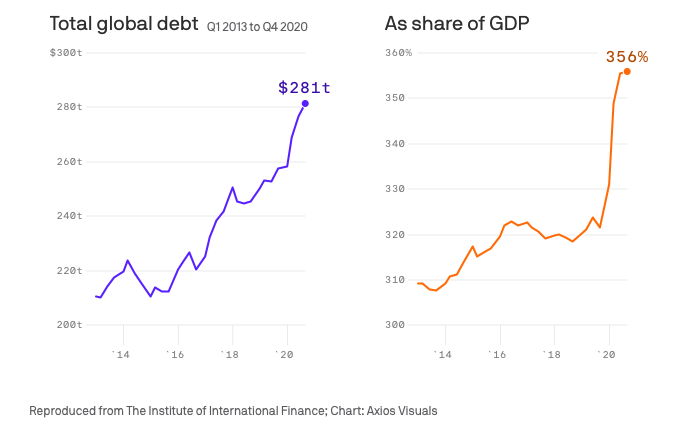

Total (Govt+Private) Global Debt now stands at a staggering 356% of GDP. We’ve never been here before- we are now navigating uncharted waters. The next bailout will have to be bigger- a LOT bigger.

The financial crisis was the beginning of a debt avalanche- it’s likely that over 70% of the major banks, mortgage brokers, and other financial institutions would have gone bankrupt, superseding the Great Depression-era record of 30%. Thousands of private and public companies would have gone bankrupt. Real estate and equity markets would have entered a freefall lasting for years, and unemployment would likely have spiked past 30%, bringing back the soup lines not seen since 1936.

Instead, policymakers kicked the can up the stairs- they issued massive amounts of government debt to paper over the 2008 crisis, and incentivized excessive borrowing in the private sector. The fundamental factors that caused the crisis (unregulated derivatives, bank combinations, excessive leverage, lack of oversight) were never resolved. As u/Criand so elegantly puts it, 2008 never ended. Now, with US Government Debt standing at over $31 Trillion, there are only tough choices ahead. We will soon reach a point where the interest payments alone on the debt supersede all US Tax Revenues- when that happens, we will have traveled beyond the event horizon- there will be no coming back. The debt will be IMPOSSIBLE to pay off. (This is according to the government’s own projections!)

The US Government continues to borrow- running a staggering $2.1 Trillion deficits for just the first half of 2021– day by day, we are adding snow to the mountains above our village. When will end is anyone’s guess, but borrowing more will only make the end worse.

Conclusion

The debt crisis will return, but this time, it will be the financial system, US government, and indeed the ENTIRE world economy that needs a bailout- and who has a big enough balance sheet to absorb that? The only answer is the ones with an infinite balance sheet- the Central Banks. The idea that anyone can borrow forever, or print money forever, with no consequences, defies basic financial logic. Impossible Objects cannot exist forever. History shows deadly consequences for the nations that venture down either path. The United States is no exception.

The Fed has already tried to escape this trap in 2018. It failed. Sovereign creditors are losing faith in the US Treasury, and have been since 2015. The walls are closing in, and the ultimate decision must be made. The avalanche is coming either way- and we only have two choices. Either we allow ourselves to be buried under a mountain of hyper-deflation, creating a new Great Depression, frozen credit and equity markets, and massive bank failures- or, we burn our way out, using the inferno of money-printing and hyper-inflation.